Financial aid repayment is confusing, to say the least. I worked in education for over 16 years. For many of those years I was counseling incoming students about financial aid, but I still couldn’t tell you the difference between Pay As You Earn and Revised Pay As You Earn without digging back into my research.

When I entered grad school I had three and a half years of student financial aid counseling under my belt. But the process was still confusing and contradictory. There was no one to turn to for strategies or solutions, only people who told me what to sign when it felt like I needed to borrow more.

Many schools offer a financial aid representative to help graduated students through student loan repayment, but if there was someone at my school to help me when I finished my graduate program I didn’t know who they were.

If you’re wading through the complexities of student loan repayment, I’m sharing my story and some simple information that can help you make the right decisions for your financial future.

The Difference Between Pay As You Earn and Revised Pay As You Earn and Other Scary Stories

What Is Obama’s Student Loan Forgiveness? And Other Confusing Ideas on the Internet

Revised Pay As You Earn and Other Loan Fundamentals

Is Student Loan Forgiveness a Dream or a Reality? My Personal Student Loan Story

Public Service Loan Forgiveness (PSLF): The Trials and Tribulations

My Loan Forgiveness Advice

What Is Obama’s Student Loan Forgiveness? And Other Confusing Ideas on the Internet

For one thing, Obama’s Student Loan Forgiveness isn’t a program, it’s what some people call programs, like Pay As You Earn that came into being during Obama’s time in office following the Great Recession.

These new programs were an attempt to address the mounting student loan debt program problems in the United States, unlike PSLF, which was to help stimulate public sector hiring. They can be confusing because many of them sound alike. Others are confusing because they are acronyms for terms that most people don’t use every day.

For example, I have a statement in my pile that says my loan types are CONS and CONU. What does that mean? It turns out these are internal codes that Nelnet uses to differentiate between loans. Not so helpful for me.

Every time I see something like that, I put my student loan docs on a pile labeled: “To Do Later. Not Now. Later.”

Revised Pay As You Earn and Other Loan Fundamentals

Let’s talk about all the different types of federal loans first.

The Federal Family Education Loan (FFEL) Program covered loans for students who borrowed student loans before July 2010.

Loans under this program included:

- Subsidized Federal Stafford Loans

- Unsubsidized Federal Stafford Loans

- FFEL PLUS Loans

- Consolidated Loans

Current federal loan types include:

- Direct subsidized federal loan

- Direct unsubsidized federal loan

- Direct Grad PLUS loan

- Direct Parent PLUS loan

- Direct Consolidation Loan

This article about the history of federal loan type changes was interesting and useful to me. It helped me understand how private lenders got involved in the loans I borrowed for school.

Now let’s talk about the latest repayment options.

Income-Driven Repayment Plan

Income-driven repayment is an umbrella term that covers four different repayment options with a 20-25 year timeline for loan forgiveness. It covers these four programs:

1. Revised Pay As You Earn Repayment Plan (REPAYE)

2. Pay As You Earn Repayment Plan (PAYE)

This chart from NerdWallet is really helpful for figuring out whether REPAYE or PAYE is your best option.

These two aren’t connected to how much student loans debt you have, instead they connect to how much money you make.

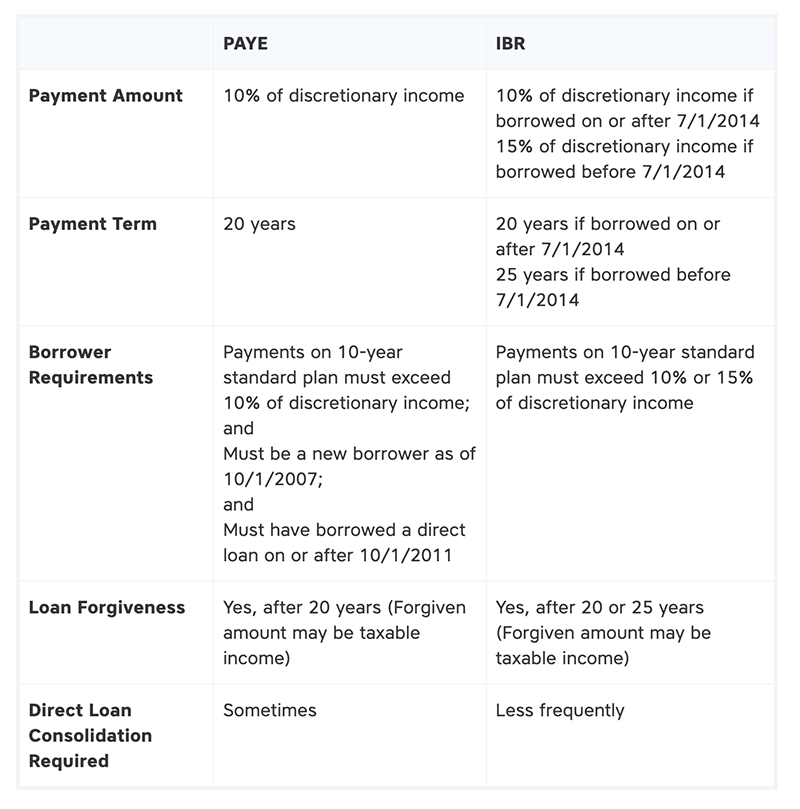

3. Income-Based Repayment Plan (IBR)

At a glance, this program looks similar to REPAYE and PAYE, but if you do some digging, this program is for borrowers who started borrowing in October 2007 or later. This chart from StudentLoanHero helped me figure it out.

4. Income-Contingent Repayment Plan (ICR Plan)

ICR is the only one of the four income-driven plans that Parent Plus borrowers can use. I honestly can’t tell what the other advantages of this program are. It seems like it makes it just a little easier for Parent Plus borrowers and the other programs are the best fit for most people.

Read more: Income-Based Repayment for Freelancers

Public Service Loan Forgiveness

Program eligibility for the Public service loan forgiveness program began on October 2, 2007.

The PSLF program forgives the balance on Direct Federal loans after borrowers in repayment make 120 monthly payments with a repayment plan and employer that qualify.

Qualifications include:

- Work full-time, at least 30 hours a week, for a government or not-for-profit organization for 10 years

- 120 payments over the course of 10 years on an income-driven repayment plan

On October 6, 2021, the government expanded eligibility so long as loan payments were made in full and on-time regardless of the payment plan through October 31, 2022.

This should make it easier for people who got contradictory information about repayment and consolidation to have a chance for loan forgiveness. Before this initiative, forgiveness with this program was shockingly low. You’ll understand why if you read my story.

Is Student Loan Forgiveness a Dream or a Reality? My Personal Student Loan Story

This system is a mess, honestly. Huge companies bought and sold my loans three times that I know of. I consolidated my graduate and undergraduate loans with Graduate Leverage in 2007. They sold my loans to Brazos in September 2010. Brazos sold those loans to Nelnet in September 2013.

I consolidated in 2007 so that all my payments were going to the same place in one clear monthly payment. I thought that I consolidated my loans, but consolidation means different things to different organizations.

When I consolidated the first time I wasn’t thinking about FFEL or loan forgiveness. I was trying to figure out how to make my tight budget easier to understand and manage. You’re not thinking about 10 years down the road when your budget looks like this:

Fast forward to 2014 I got one of those flyers that looks like a scam in the mail. I was getting so many that I decided it was worth looking into and they talked about options that sounded good. So, I called my loan servicer, Nelnet, looking for options to lower my monthly payments. Living in San Francisco in 2014 meant very high rent, and during that conversation, we discussed income-based repayment and graduated repayment options.

I was under the impression that shifting to income-based repayment meant that I was also making payments toward Public Service Loan Forgiveness. I made every payment on time and reached out to my loan servicer whenever something looked wrong. But I was seriously mistaken.

In February 2017 I called to check in on my repayment plan and details. That day I spoke to someone who outlined what I would need to do to be eligible for student loan forgiveness in detail.

At this point, I thought I had made a significant lump of payments toward loan forgiveness. I was feeling stuck in my career and wanted a change.

That one phone call kickstarted my plan to get out of the nonprofit world. If I was just a few years away from loan forgiveness, I would have stayed. But hearing that I was 10 years away was a devastating blow.

From 2014 to 2017 my on-time payments weren’t eligible for PSLF. Those years are on top of years of on-time student loan payments before Obama’s student loan forgiveness programs existed. I have a perfect loan payment record. I spent nine years working for nonprofits since the creation of the PSLF. But I’m not eligible for forgiveness for any of my $89,614 in federal student loan debt. As of today, I’ve paid almost $120,000. The numbers don’t add up.

What it means to manage student loan debt today

I think my challenge is what life management requires today. We live in a world where most parts of life involve complex systems. To succeed we need to learn, understand, and constantly update our knowledge as industries, business processes, and technology evolve.

Most of us experience this at work. Say you work with 10 to 20 different applications. Each one changes or updates every month or so. You’re constantly learning and navigating new systems. At work it’s frustrating, but you work 40 hours a week. You make time to learn so that you can keep your job.

But this level of complexity also comes into retirement. Healthcare. Figuring out what food to eat. Where to live. And managing student loans.

Sometimes this level of complexity means that you’ll be asking the wrong questions during a phone conversation. It means that you won’t quite understand the fine print. This issue isn’t due to customer service, though they are the easiest to blame.

Customer service teams have thousands of details and data points to learn, memorize, and apply to thousands of unique conversations. So it’s not realistic to expect them to tip us off to every change that we could take advantage of.

Unless you are always on top of everything, there’s a chance something will go wrong. There’s always a chance that you’ll pay more than you could or should have. And there are systems that are banking on that.

It’s exhausting to be wary and alert all the time. I have too many things that I want to do and only so much time. Because of this, my financial health often suffers.

Public Service Loan Forgiveness (PSLF): The Trials and Tribulations

I can’t remember when I first heard about the Public Service Loan Forgiveness program. It always felt like a distant dream, something for someone else and certainly not me.

I don’t know why I didn’t investigate this program on my own or immediately reach out to one of my friends in Financial Aid. I think I didn’t trust it. I didn’t think that it would last long enough for me to benefit from it. Then after all that mess in 2017, I decided to shift gears and put my student loans at the back of my mind.

Then a few months ago a friend from grad school reached out for help naming her most recent body of work. We had a nice long phone conversation that stumbled into the latest development of the PSLF.

That until October 2022 the federal government will push through applications for the PSLF program even if they didn’t consolidate their loans correctly, massively expanding eligibility for the program. My stomach dropped when I heard this.

I am so frustrated because those eligibility requirements and my inability to meet them were the biggest push for me to leave my work in art education in 2017.

A few days later I reached out to my loan servicer to try and figure out what my options were and who I should talk to.

According to my records, I’ve made 148 student loan payments, but I’ve only made 36 payments on Revised Pay As You Earn. According to their records, I have 84 remaining payments out of 120. That just didn’t make any sense to me. I asked them to check again, and they said I made 43 student loan payments before consolidating to Revised Pay As You Earn. They only counted the payments that I’ve made through Nelnet.

My understanding from Nelnet is that none of the payments I made prior to reconsolidation in 2017 are eligible for Public Service Loan Forgiveness because they were commercial loans. But according to some of the reporting on PSLF, the new changes include FFELP loans. So, my latest investigation into my eligibility for student loan forgiveness ended with a frustrating phone call.

I completed the form, and my loans are currently in forbearance like most everyone else because of COVID. I am getting confirmation from the nonprofits I’ve worked for in hopes of potentially working toward forgiveness at some point. Clearly, I’ll need to do some more research.

My next step is to call the Department of Education student loan support line. The number Nelnet gave me is 1-800-557-7394. The person giving me the number didn’t know if it was a general number or not, so that’s helpful.

I’m organized enough that I’m going to continue to investigate and see what is possible for me with my student loans. My student loan debt is why I can’t afford to buy a house. It’s why my future feels precarious. I may go back to the non-profit world someday. It would be great to pay off my loans 10 years early, but I may just dig into what I’m responsible for and see if I can do anything else that can help me feel less helpless about my debt.

Read more: Get Paid for Art? Is That Still Possible?

My Loan Forgiveness Advice

Clearly, I am not yet a financial expert. I couldn’t even figure out my income taxes on my own this year. But with what I know at this point, there are a few tips I can share.

1. Talk to whoever you can about your personal situation

I didn’t reach out when I could have and that’s meant a lot of missed opportunities. Talk to the Financial Aid Office at your school, a financial advisor, parents, friends, and colleagues.

2. Save everything!

I didn’t save my paper records for every student loan payment I’ve made since 1999. I’m not sure how to get these records.

I understand that you’re supposed to save tax records for 3 years and I’ve always done that. I’ve also shredded and disposed of them properly. But it never occurred to me that I would need to save over 20 years of loan payment records to get a clear sense of my payment history because of the buying and selling of my student loans.

I didn’t know this was a common practice. I didn’t realize I would need to hold on to all of this paperwork to understand the history of my student loans payments, interest rates, and different loan and consolidation types. But here I am, with little to no record of my loans prior to 2013. I can only trust the huge bank that services and makes a profit on my loan payments, which barely make a dent in my interest, let alone the principal of my student loans.

In 2010 I did a comprehensive purge of all my paperwork. I purged again in 2017. It just didn’t make sense to carry around a bunch of paper. I wish I’d saved it all just so I could figure out what is really happening with my student loans and my best strategy for moving forward.

3. Write everything down

I take handwritten notes during personal business calls. In my notes, I include the date and time of the call and the name of the person I spoke to. This is it been helpful with phone bill refunds and utilities. When it comes to dealing with my student loans this strategy has been less successful, probably because it’s hard to keep track of random handwritten notes spanning 22 years. It’s also because I have horrible handwriting.

4. Find an app

There are many tools for businesses to pull their data from a single source of truth. This makes it easier to keep all the data in one place for comparison, measurement, and noticing anomalies. As far as I know, there’s nothing like that out there for individuals to manage their finances. It would be amazing to have a tool that automatically tracks the different elements of my personal finances instead of 5-10 different apps and websites. So, I’ll be looking into this soon.

5. Look into alternate sources of income

Traditional Financial advice when I was in my 20s said not to invest until you’re debt-free. Today’s advice on investing while in debt is all over the place. I won’t be debt-free until I’m almost retirement age, so I’ll be looking into investing now too.