A year after finishing grad school I walked the four miles home from work each day to save the $2 I would have spent on bus fare. Four years later, I was able to afford a studio apartment in San Francisco. My personal financial stories are a rollercoaster, to say the least.

I’ve paid off over $50,000 in credit card debt, over $100,000 in student loan debt, and another $6000 in healthcare debt. I still have over $100,000 in outstanding student loan debt.

Money management was never my strength. I understand the fundamentals, but I’ve always been better at spending money. My parents used to call me a princess because I was born with expensive taste.

Personal Financial Stories From an Artist

My Personal Money Story

Student Loan Debt, Part I

Credit Card Debt, Part I

Parental Debt

Car Debt

Student Loan Debt, Part II

Credit Card Debt, Part II

Repaying My Student Loans

Career Change

Healthcare Debt

Freelancing and Entrepreneurship

Early financial stories

There’s a story my mom used to tell from when we moved from Oregon to California in 1986. I was in 3rd grade.

She and Dad found the house that we would be renting. To plan how our furniture would fit so we wouldn’t haul anything we didn’t need down there, she asked me to help as she marked out the floor plan of the house with graph paper, then cut out our furniture to scale. When we finished our house planning, she asked which bedroom I wanted. “I would want the master bedroom” was my prompt reply.

Money always felt a bit abstract to me. I understood we needed it to pay bills, but without specifics of those bills, I just assumed there was always enough. I didn’t understand all the juggling that my parents did to make it work.

They would let me know when something I wanted was too expensive. For example, when I wanted to go on a cheerleading trip they couldn’t afford I borrowed the money from my grandpa. They helped me create a little ledger to track my repayment.

But I didn’t want to put off the fun stuff just to save money for later. If I went to the mall, I wanted an Arby’s beef and cheddar and a jamocha shake. I didn’t want to save money and eat at home.

My Personal Money Story

Once you read my money stories there’s a possibility that you will question the rest of my knowledge and advice. It’s not pretty, and it took a long time for me to face it and deal with it.

I’ve always had a chip on my shoulder about wealth, the stock market, and investing. The only thing investors seem to make is money and they make an insane amount of it.

An average stockbroker makes $55,000 in their first year on average. A few months ago I pulled up my annual earnings for my first year working full-time. I made $8,750. I have spent my entire adult life stressed about money and I am so tired.

It’s also hard because of my identity as an artist. The world at large seems to think artists don’t know how to change their own pants. It makes me crazy because a significant percentage of the artists I know are not only highly intelligent and organized, they are innovative critical thinkers.

A big part of starting this blog is talking about personal finance for artists. I want the world to be a more just and equitable place than it is, and I strongly believe that part of that is funding for artists. Until that happens, I’m going to use this forum as a tool to learn more about my options in the financial world, and to share my journey as I do.

Student Loan Debt, Part I

My personal money stories start in high school in San Diego, CA. I was a cheerleader and took AP classes. My parents were okay with me not working a job during high school because I was so busy with school activities.

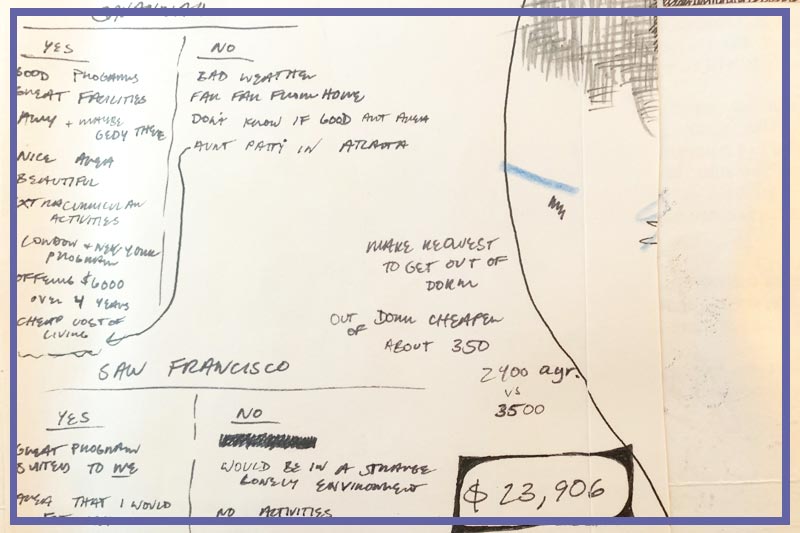

When I applied to art schools for college, and we got into a lot of arguments because they were against it for financial reasons– it was too expensive.

I’m very stubborn. We argued through the summer after high school graduation as I bagged groceries at a local grocery store. The fights continued into fall, when I got a retail job at an art supply and framing store.

I made a deal with my parents that I would save all my earnings to cover art supplies during my first term at our school. They agreed to take out the Parent PLUS Loan to cover living expenses and the remaining tuition for my first year at art school in Savannah, GA.

Personal financial stories from college

It took a while to get to this agreement so I started college in January instead of in the fall. I enjoyed school and continued to work in art retail and framing during the winter and summer breaks through my sophomore year of college.

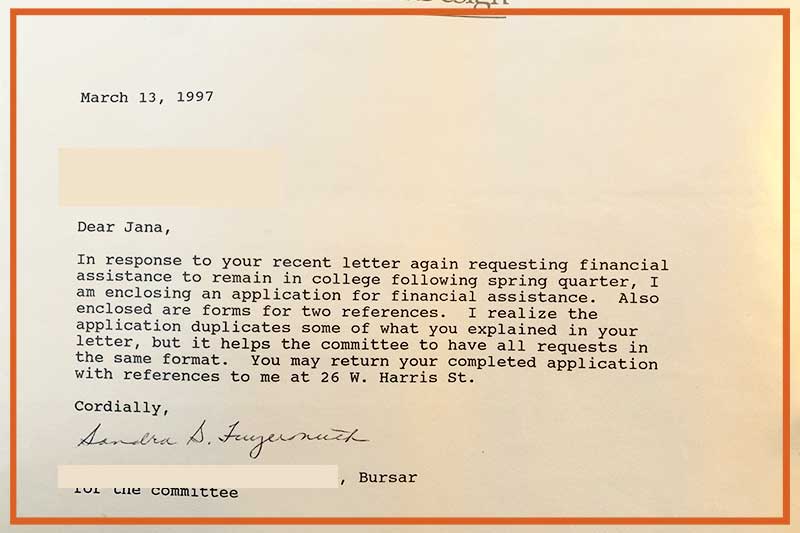

For most of my sophomore year, I was stressing about everything, including my health, which involved several visits to the ER. I also stressed about continuing school, because my parents made it clear that they would not be able to take out loans for my final two years of college. This was partly because my mom was having health issues too.

I had a work-study job in the admissions office at my college and made friends with the women I worked with. One of them, Melissa Blackman, went out of her way to help support me. She asked about extra scholarships from the school on my behalf. With her help, I received access to an application that earned me a scholarship covering tuition, room, and board for my last two years of college.

I did a paid internship that summer, but the income for it barely covered the gas for my commute. When I started school in the fall of my junior year there was an issue with my refund check that took more money out of my pocket.

Second half of college

I lived in the dorm junior year and continued to work 16-20 hours a week. I worked in the same art retail store during my winter break, but my parents moved to Reno, NV that spring. My summer internship fell through at the last minute, so I got a data entry job through one of my dad’s friends.

My credit card debt started climbing at that point. I tried to keep my balance at zero, but cross-country flights to school and other flights to see my friends after my parents moved started to dig a hole in my credit card balance.

The hole got deeper the following summer when I did an off-campus trip to New York. I purchased a large portfolio and professional digital prints of my work for jobs to build my portfolio for job applications. It was expensive but necessary. I let loose at the end of my senior year and made plans to move to San Francisco to live with my sister after college graduation.

Credit Card Debt, Part I

I moved to San Francisco in early July and quickly found a job in a framing shop but I got fired a week later. There was always a feeling of terror about my student loans. I knew I didn’t have to start making payments until November because I graduated in May, but the idea of that much debt was horrifying. San Francisco was also having an expensive moment. This was 1999, just before the .com bubble burst.

I decided to live with my parents while I built my career as an illustrator and graphic designer. I was lucky and found a job pretty quickly. My mom taught me a crazy trick, calling every design shop in the phone book. Using that strategy I happened upon a great design shop in Reno. The first project I completed with them was honored in the Communication Arts Regional Annual.

After a few months, I realized that I didn’t love graphic design and the repetitive work it took. I decided to do a travel program in London called BUNAC. My plane took off on January 2, 2000. I had a panic attack shortly after arriving and instead of staying in the UK for six months, I stayed four days. That decision ticked up my credit card debt with international charges for food, long-distance calls, and airfare.

Don’t use a credit card for groceries

By February I’d moved back to Savannah, GA and I lived off my credit cards for two months. My entry-level salary barely increased in the three and a half years I worked there.

I racked up $23,000 in credit card debt before I decided to do something about it.

My biggest expenses were $350 a month for rent and $250 a month for car payments. I bought my little Chevy pickup to feel safe going places at night, but there was a key missing from the flywheel, so it didn’t always start.

With some persistence, some painting sales, and credit consolidation I got my credit card balance down to $5000. Then I decided to move to Portland, OR in 2003.

Parental Debt

My parents were generous enough to cover the rest of my credit card debt while I figured out what life would look like in Portland. We made an agreement that I would pay them back at 2% interest. We didn’t agree to the timing for repayment, but we should have because I wasn’t done being stupid about money.

I worked a temp job for my first eight months in Portland, then my position turned into a full-time role. I worked a lot of overtime. You would think that I would have been able to save some money at that point, but when I push myself too hard I just want to spend money.

Car Debt

Eating out, drinking, clothes, travel– they’re what lights me up when I’m stressed and a big pitfall when I’m trying to save money. I have also made some quick and not-so-bright decisions around money.

Case in point– I thought I needed a car in Portland because the guys I originally lived with chose a neighborhood with a long commute to my office.

I bought a used Honda Accord with a moon roof for $9000. A few weeks later found an apartment of my own just ten blocks from the office. I got hosed at the car dealership. I didn’t want to admit that I didn’t understand the terms while I was wrangling with the salesman.

Not only did I not need a car, but my car payments were also over $450 a month. I exercised it once a month like a fancy horse and the battery died twice from lack of use.

Student Loan Debt, Part II

I wasn’t happy in Portland, so I applied to grad school in San Francisco, plunging myself into another $120,000 in student loan debt. This was on top of the $18,000 I had left in student loan debt from my undergraduate degree.

I worked at Starbucks for 3 hours before I quit. The hope was that a part-time job would help me continue to make my car payments. I decided to sell the car instead and the price I was able to get exactly covered what I needed to pay it off.

Credit Card Debt, Part II

During grad school, I continued to live the same way I had in Portland, but I wasn’t making an income. By the time I finished my two years of graduate school I had over $25,000 in credit card debt.

My last month of grad school was especially stressful. I knew that even if I started a new job the day after I finished school I wouldn’t have enough in my account to cover rent.

I ended up taking out a $5,000 personal loan, but still missed one minimum payment for my Discover card. That mistake drove the interest for that card from 2% to 18%. It was rough.

I changed jobs four times in the next four years and I moved five times from 2008 to 2012:

- From San Francisco to Los Angeles

- Los Angeles to San Diego

- San Diego to San Francisco

- Then from San Francisco to Marin

- And back

Moving isn’t cheap

I spent five months of the Great Recession unemployed. I used the same credit consolidator again to pull all my credit cards into a single monthly payment and to negotiate my sky-high interest rates. The money I’d been saving for a car, clearly a necessity in Los Angeles, had to be spent to continue to pay down my credit cards.

I had a disastrous relationship that cost me a big security deposit and gutted my savings. Luckily I found an apartment where the owner accepted a security deposit in installments.

By December 2011 my credit card debt was gone

I haven’t had an outstanding balance on my credit card since. I learned a rule that helped during that time– if something isn’t worth twice the asking price it’s not worth putting it on a credit card. So I don’t.

For the eight years that I lived in the Bay Area my savings was what I had left of my income tax return after vacation. I used my meager savings to cover my small overages each month, living just beyond my means, always. I don’t think I ever had than $200 in savings at any given time.

Repaying My Student Loans

My personal money stories have been pretty rough up to this point, but it may seem like I finally have a handle on my finances. Alas, no.

I thought I was on the right track with my student loan debt. I’d worked for a non-profit from 2010 to 2017, so I thought I was on the path towards forgiveness for my Federal student loans, and I was repaying loans with the new income-based repayment option.

I’d had many conversations and assurances from my loan servicer that I had consolidated my student loans in the right way for Public Service Loan Forgiveness eligibility. But it wasn’t true. I discovered in February 2017 that I had to reconsolidate again to be eligible for the program, losing years of progress toward that goal.

What I thought was at least four years of payment toward the mandatory ten years was down the drain. I decided to make a dramatic change and shift my career from art school admissions to writing.

Career Change

I didn’t know what kind of writing I wanted to do professionally, but I knew that I couldn’t afford to figure it out while I was still living in San Francisco. So, I moved back to Portland in December 2017. I talk about the process I went through to change careers in Not all who wander are lost: How to change careers after 40. Even though it took me five months to figure out a new career, I’ve had a safety net in my savings account since 2018.

Healthcare Debt

The debt I’ve accumulated and paid off from 2018-2021 is due to the ridiculous American healthcare system.

I took a trip to the emergency room in 2018 after the nurse from the phone service told me that my symptoms sounded like appendicitis. They didn’t find anything, and that visit cost around $2600.

A couple of years later, more stomach issues meant an upper endoscopy to see what was going on in my gut, netting a collection of ambivalent test results and $3000+ in healthcare bills. I spent over $600 in doctor’s appointments and prescriptions in 2020 and another $1020 in 2021 for women’s health issues.

Each time I spoke to the provider about breaking the bill into manageable monthly payments, so the debt was manageable. But it’s rough to spend that much money just trying to figure out what is going on with my health. It makes me resistant to going to the doctor at all.

Freelancing and Entrepreneurship

I’ve come to the conclusion that the best option for me Isn’t to spend less, it’s to make more.

I’m working towards a new goal. I’m going to figure out how to earn $10,000 a month, every month. And I’m not going to hustle. I’m going to continue to take time to work out, spend time with my family, and make time to rest!

As I test ideas and learn new strategies as a freelancer, entrepreneur, investor, and whatever else I’m going to talk about it here on this blog. Artists deserve money, and that includes me!

Keep reading, and I’ll keep you posted.